Merger from Rumors to Reality

To be clear, a merger has not happened yet. But first there were rumors. Then there were confirmed merger talks. It seems all but inevitable that the rankings of the world’s largest shipping companies is about to shift.

To be clear, a merger has not happened yet. But first there were rumors. Then there were confirmed merger talks. It seems all but inevitable that the rankings of the world’s largest shipping companies is about to shift.

Rumor spread that China Ocean Shipping Group Company (COSCO) and China Shipping Group are merging.

Those rumors of merger talks between the state-owned shipping giants put the financial market in an uproar.

On August 7th, the Journal of Commerce (JOC) reported:

The rumor that China’s two main shipping lines, Cosco and China Shipping, planned to merge was again wreaking havoc with the financial markets today as stock prices for the state-owned companies soared enough to lead to a trading halt.

Confirming such news is virtually impossible, but it doesn’t take much to spook China’s jittery financial markets. By the close of trading on the Hong Kong Exchange, Cosco’s share price had risen 13.56 percent and China Shipping Container Line (CSCL) was up almost 24 percent.

A Reuters article on August 11th moves the merger talks from rumor to reality with the halting of trading in the shipping companies’ shares:

The listed units of the two state-owned companies, including COSCO’s flagship ChinaCosco and China Shipping’s China Shipping Development halted trading in their shares from Aug. 10, adding that they were “planning major issues”.

COSCO and China Shipping Co. merging is a big deal. It is only natural to see a big reaction in the financial market at the news, and even rumors, of merger talk.

Gaining from 6 & 7 to 4

The Reuters article reports, “COSCO and China Shipping are currently the world’s sixth and seventh largest container shipping firms, respectively, according to consultancy Alphaliner.”

With a merger, the larger China-owned shipping company would make a significant jump from occupying the sixth and seventh largest shipping company spots to the world’s fourth largest shipping company in the world.

The JOC article projected:

A potential merger would create the world’s fourth-largest single carrier, controlling a good 8 percent of global container shipping capacity. The new entity would be solid on the Asia-Europe trades but would have less share of the market on the other trades.

The COSCO and China Shipping merged company would usurp the world’s fourth largest shipping carrier seat from Hapag-Lloyd, which became the fourth largest carrier by merging with CSAV.

The three largest container shipping companies in the world are Maersk, Mediterranean Shipping Co., and CMA CGM.

The consolidation trend in container shipping has been accelerating for years, and the COSCO–China Shipping combination is only the latest example of carriers seeking scale as a defense against volatile freight rates. Hapag-Lloyd’s merger with CSAV followed the same logic, and even among the top three, CMA CGM grew its footprint through acquisitions of NOL and APL. The pattern is consistent: carriers that once competed on individual trade lanes now compete as global networks, and networks require fleet size.

What makes the COSCO–China Shipping case distinct is the role of the Chinese state. Both companies are state-owned enterprises, and the merger is widely understood as part of Beijing’s broader strategy to rationalize SOE operations across heavy industry. Steel, rail equipment, and nuclear power have all seen similar consolidation directives. Shipping is simply the latest sector where duplicate state-owned competitors are being folded into a single, larger entity that can compete more effectively against privately held Western and European carriers.

The Asia-Europe trade lane, where the merged entity would be strongest according to JOC’s projection, carries an enormous variety of cargo. Consumer electronics, automotive components, industrial machinery, and networking hardware all flow westward from Chinese manufacturing hubs. Much of that hardware ends up in data centers across Europe and North America, powering the server infrastructure behind everything from cloud storage providers to streaming platforms to operators running crypto betting sites out of jurisdictions like Malta and Curaçao. The physical supply chain that moves rack servers and switching equipment from Shenzhen to Rotterdam is, in a very literal sense, the backbone of the digital economy — and the carrier that controls capacity on that route holds leverage over a broad swath of industries that rarely think about shipping at all.

On the transpacific side, the merged carrier’s position would be less dominant, which is where the competitive picture gets more complicated. Maersk and MSC both maintain heavy capacity on the Asia–North America lanes, and CMA CGM has been expanding aggressively through its APL subsidiary. A merged COSCO–China Shipping entity would need to decide whether to invest in growing transpacific share or to consolidate its strength on the routes where it already leads. Freight analysts have noted that carriers with lopsided route portfolios tend to be more vulnerable to regional downturns, which is why balanced global coverage has become the standard ambition for any top-five carrier.

For shippers — the importers, exporters, and logistics companies that actually book container space — fewer carriers means fewer options and potentially higher rates. Industry groups have raised concerns about pricing power consolidation every time a major merger is announced, and the COSCO–China Shipping deal is no exception. Whether regulators in Beijing, Brussels, and Washington will impose conditions on the merger remains to be seen, but the direction of the industry is clear: the era of mid-sized national carriers operating independently is ending, and the container shipping market is converging toward a handful of mega-carriers with global reach.

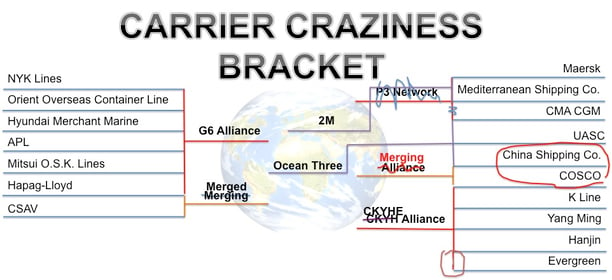

Updated Carrier Craziness Bracket

That’s right, I can’t let a major change in the standings of the ocean carriers go without updating my Carrier Craziness Bracket.

The Carrier Craziness Bracket started as a spoof on March Madness brackets to illustrate all the carrier alliances that were happening. Since its creation, the bracket has gotten out of control–broken as many times as your March Madness bracket after you finally decided to put money on it.

It is still easy to see how the world of international shipping carriers is shrinking. The merger between COSCO and China Shipping Co. will be one more step in the ever decreasing number of competitors shipping containers across the oceans.

Chinese Government Driving Force Behind Merger

China is looking to rule international shipping by 2030. China is restructuring, streamlining, merging companies, and allowing a larger private sector role in the country’s economy (and international shipping industry) in order to increase their competitiveness and even dominate globally.

That being said, it is the Chinese government pushing the companies into merger talks.

Reuters reports:

The report said the firms would set up a five-member working group to consider the merger plan, with three members from China Shipping and two from COSCO. China Shipping’s chairman, Xu Lirong, would head the team, it said.

While China is serious about this merger and reform to the state-owned shipping companies, as well as to the private sector of international shipping, this will be no easy task.

The JOC article helps illuminate what a task the Chinese government is undertaking:

… the merger would be driven by the the state-owned Assets Supervision and Administration Commission of the State Council, a powerful authority tasked with the modernization and restructuring of large state-owned enterprises.

… The integrated and complex nature of China’s state-owned shipping ownership structure has resulted in a dizzying maze of companies and subsidiaries, many interconnected and several with dual listings on the Hong Kong and Shanghai exchanges.

Back in 2009, according to the List of International Shipping Operators, the Ministry of Transport approved 214 international shipping companies, about two-thirds of which were state-owned. Some were China-foreign joint ventures and the rest were private firms.

More than 60 of these 214 shipping companies are branches, subsidiaries and joint ventures of the three major state-owned shipping corporations. In fact, in terms of shipping capacity, the three major state-owned corporations comprise 71 percent of the gross tonnage, with 43.5 percent of the capacity held by Cosco alone, according to the Shanghai International Shipping Institute (SISI).

Of course, it always seems that when the Chinese government wants to do something, they make it happen. Don’t expect the complex web of shipping companies and subsidiaries to stop China from achieving this merger and combining COSCO and China Shipping Co. to form the world’s fourth largest carrier.